Changes to the Tax Holiday Program for Foreign Researchers and Foreign Experts

The Ministère de l’Économie et de l’Innovation (MEI) recently announced changes to the eligibility criteria for the Tax Holiday Program for Foreign Researchers (FR) and Foreign Experts (FE). This program is designed to facilitate the recruitment of foreign researchers or foreign experts capable of aiding in the commercialization of innovation activities or the advancement of technology, respectively, within private companies in Quebec. Quebec companies remain competitive by attracting highly qualified researchers/experts to perform scientific research and experimental development (SR&ED).

What’s New?

1. The tax holiday is applicable as of the date of hire on contract.

The tax holiday is now based on the hiring date and the number of months that pass after this date, rather than in calendar years following the year in which the hiring date fell – making it much more beneficial. If a candidate is hired October 9, 2021, the tax holiday begins on October 9, 2021, and lasts for 60 months, i.e., October 9, 2026.

2. Applications must be submitted prior to moving to Quebec.

The rules also state that candidates now need to apply before their arrival to Québec. This means that employers should apply prior to the candidate’s hiring date and arrival into Québec. Those who are already in Québec and that have not yet applied should move forward with applications as soon as possible to avoid any issues. These changes are on-going and may be further refined in the next couple months.

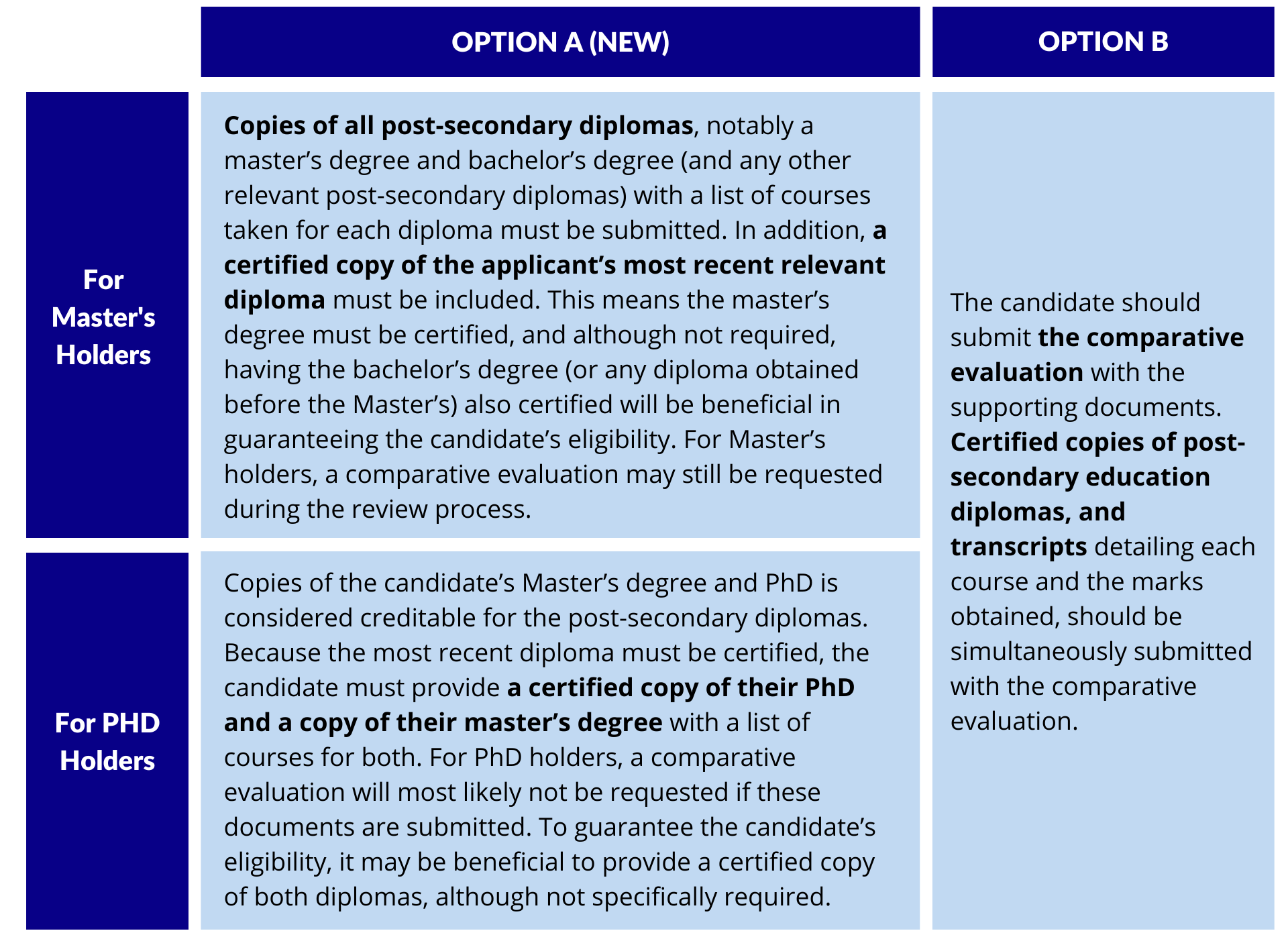

3. The comparative evaluation requirement has been updated.

Previously, the approval of the tax holiday depended on the receipt of the comparative evaluation certificate. Going forward, the comparative evaluation may not be required for approval. However, it may be requested during the review process on a case-by-case basis; it is therefore recommended to apply in advance to minimize the processing time as the comparative evaluation issuance process is the longest part.

One of the following documents must now be submitted with the tax holiday application:

- Copies of post-secondary diplomas with a list of courses taken for each diploma and a certified copy of the applicant’s last relevant diploma, OR;

- Comparative evaluation of studies completed outside Quebec issued by the Ministry of Immigration, Francisation and Integration (MIFI) and sent directly to MEI

4. No annual renewal is required for FRs, but it is still required for FEs.

Foreign researchers only need to submit one application to receive the full tax holiday, no longer needing to submit annual follow-ups. For foreign experts, annual renewal applications are still required for the five-year duration of the tax holiday. Once the initial expert certificate has been issued and the candidate is employed in Québec, the employer must submit an annual application for the expert certificate annually before March 1 of the calendar year following the tax year for which the applicant is taking the tax holiday.

Additional information on the comparative evaluation

Along with the comparative evaluation document, the candidate should include certified copies of all post-secondary diplomas they wish to have evaluated by the Ministry, noting that the minimum education requirement for the tax holiday is a graduate degree for foreign researchers and a first cycle university degree (bachelor’s) for foreign experts. If you would like to learn more about the tax holiday program requirements, please read our previous article.

To find recognized authorities to certify your degree as a true copy please see the List of authorities recognized by the Ministère for certifying documents. It explains how to obtain a certified copy of your diploma depending on the country or territory where your documents were issued. A copy certified by the issuer of the document (your university) is always the preferred format.

Further reading

- Tax Holiday Guidelines – Foreign Researchers and Foreign Experts, official PDF guidelines from the MEI

- Tax Holiday for Foreign Researchers, MEI website

- Tax Holiday for Foreign Experts, MEI website

If you have any questions about the Tax Holiday Program that this blog post left unanswered, or if you are considering submitting a claim, don’t hesitate to contact our team at: 1-800-500-7733, ext.102.

Disclaimer: The views expressed in this article are provided for informational purposes only. It is not intended to nor can it replace the evaluation of your specific tax credit claim by a dedicated consultant.

")