SR&ED FAQ: How Does SR&ED Work in Canada?

Mar 1, 2018

As experts in the Canadian Scientific Research and Experimental Development (SR&ED) Tax Incentive Program, we often find companies have a basic understanding and appreciation of the program, but still require clarification on certain aspects. We’ve identified the most common questions companies have with regards to eligibility, application, and review of their SR&ED files.

1. What is the SR&ED Tax Credit Program?

Simply put, the SR&ED tax credit program enables foreign-controlled and Canadian-controlled companies to earn investment tax credits on qualified expenditures either in the form of a cash refund, a reduction in taxes paid, or both.

Companies qualify if they have performed eligible research and development (R&D) to create a new product or process or improve an existing one.

2. What can I claim under the SR&ED tax incentive?

Here is a short list of expenses that can be compiled when calculating total credits owed to you:

Salaries and wages

Materials consumed or transformed

Subcontracting fees

Overhead

Prior to 2014, capital expenditures, such as new equipment and machinery were eligible for SR&ED credits. Since then, they’ve been eliminated from the program, but may be deducted from business income as a depreciation expense.

3. What do I have to do to get the tax credit?

To qualify, you need to be doing one of three activities:

Experimental development – attempting to achieve technological advancement

Applied research – attempting to advance scientific knowledge with a specific and practical application in mind

Basic research – trying to advance scientific knowledge, but with no practical application in mind

Fun fact: Most SR&ED claims fall under the experimental development stream.

Moreover, any work that directly supports the main R&D activities above is also eligible.

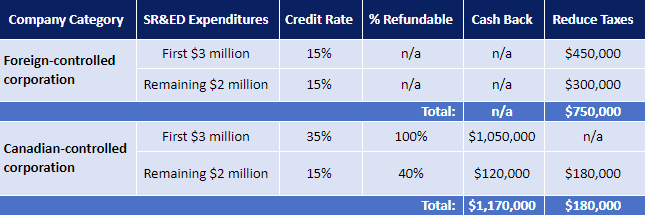

4. What is the maximum tax credit rate?

Federally, the credit rate depends on two factors:

Is the company foreign controlled (Canadian subsidiary of a foreign parent) or is it Canadian-controlled?

Do you have more or less than $3 million in eligible SR&ED expenditures?

Below is a summary of maximum federal credit rates for a fictional company with $5 million in eligible SR&ED expenditures:

Source: Government of Canada

Recall that the above figures only reflect federal rates. To see how provincial rates are added, please contact our funding experts for a free consultation.

5. As a founding member of the team, can I apply the credit toward my own salary?

If the founding member owns 10% or more of the issued shares of any class of the capital stock, that founder is deemed a “specified employee”.

When claiming SR&ED for specified employees, there are two constraints:

You must exclude any bonuses or remuneration based on profits paid to founding members

Salaries are capped to a maximum of 5x year’s maximum pensionable earnings (YMPE)

6. Is there a salary cap to what I can claim?

Absolutely not. Cumulatively, however, if project costs (measured in salaries and wages) surpass a certain threshold, your refundable rate may decrease.

For example, certain corporations may earn the tax credit at the enhanced rate of 35% up to a maximum threshold of $3 million in eligible R&D expenses. Anything more than $3 million, the basic rate of 15% applies.

See question four for an example of how SR&ED rates are affected.

7. What constitutes a Canadian employee?

An eligible Canadian employee is one that is a Canadian tax resident and who is issued a T4 by the employer.

The determination of residency status generally depends on two factors: significant residential ties to Canada (i.e. a home) or secondary residential ties to Canada (i.e a car or bank accounts).

Immigration status has no real bearing on determining an employee’s eligibility. As long as taxes are being paid in Canada, foreign workers who are in Canada on a visa or who have permanent residency (PR) status are just as eligible as Canadian citizens.

8. What impact does provincial or federal incorporation have on my SR&ED tax credits?

None. While this may have an impact on branding, intellectual property, and international trade, this has no bearing on your eligibility to the SR&ED program, nor does it affect the federal tax credit rates.

9. When do I claim the tax credit?

For corporations, filings (tax returns) are due no later than six months after your fiscal year-end. SR&ED reports are due no later than twelve months thereafter, or eighteen months after the end of the tax year in which you incurred the R&D expenditures.

For example, for the fiscal year of 2018, a corporation with a December 31st year-end will have a filing deadline on June 30th, 2019 and a deadline to apply for the SR&ED tax credit on June 30th, 2020.

10. When do I get the tax credit?

CRA recently published a report on their success rates and average processing times.

Assuming you submit your SR&ED claim within a six-month time frame after your fiscal year-end, the following processing times apply upon receipt of a complete claim:

Refundable claims which have been accepted as filed, will be processed within 60 calendar days of the date of receipt.

Refundable claims selected for review will be completed within 180 calendar days of the date of receipt.

CRA reports that they achieve these service standards 90% of the time.

Conversely, if you submit your claim later than six months after your fiscal year-end, you can expect longer processing times.

11. What happens after I submit my SR&ED file?

Once your SR&ED claim is submitted, the CRA processes it as such:

The CRA will screen it and check for completeness. The goal is to determine if the file can be processed without further review.

If a review is needed, they will forward it to a coordinating group for further investigation. Otherwise, the sequence stops, and the claim is filed as is.

The group’s technical and financial officers will review the claim and will ensure that you get the SR&ED tax credit to which you are entitled.

The technical reviewer determines whether the work meets the definition of eligible SR&ED.

The financial reviewer examines the costs associated with your project(s) to make sure that they are allowable SR&ED expenditures.

The claim is then assessed, and a Notice of Assessment is sent to you shortly thereafter.

How R&D Partners Can Help

If you have questions or comments about the SR&ED tax credit program, please do not hesitate to contact Sahar Ansary at 1-800-500-7733 for more information.